Are you curious about how banks and financial institutions determine the cost of borrowing money? Then you’ll definitely want to learn more about interest rates! Understanding interest rates is a crucial aspect of financial literacy, and it can impact many areas of your financial life.

From taking out a mortgage or car loan, to investing in the stock market, to simply choosing the right savings account, interest rates play a significant role in your financial decisions.

Interest rates may seem like a dry or technical topic, but they are actually quite fascinating once you start to learn more.

Did you know that interest rates are influenced by many different factors, such as inflation, economic growth, and even the actions of the Federal Reserve? Or that different types of interest rates, such as fixed or adjustable, can affect how much you pay on a loan or earn on an investment?

By understanding interest rates, you can make smarter financial decisions, save money, and even potentially earn more from your investments.

So, if you’re ready to delve deeper into the world of interest rates and expand your financial knowledge, then read on! Whether you’re a financial novice or an experienced investor, learning more about interest rates is an important step towards achieving your financial goals.

Definition

Interest rates are a fundamental concept in finance and economics. In simple terms, an interest rate is the cost of borrowing money or the return on lending money.

It is expressed as a percentage of the principal amount and can be either fixed or variable. Knowing the definition of interest rates is essential to making informed financial decisions, as it affects the amount of money you will need to repay or earn on a loan or investment.

For example, let’s say you want to take out a mortgage to buy a house. The interest rate on the mortgage will determine how much money you will need to repay the bank over the life of the loan.

A high interest rate will result in higher monthly payments and a greater overall cost of the loan, while a lower interest rate will result in lower payments and a lower overall cost. Similarly, if you want to invest in a savings account or a bond, the interest rate will determine how much money you will earn on your investment.

By understanding the definition of interest rates and how they work, you can make better financial decisions and avoid making costly mistakes.

For example, if interest rates are expected to rise, you may want to consider locking in a fixed rate on a loan to avoid higher costs in the future. On the other hand, if interest rates are expected to fall, you may want to delay taking out a loan or invest in a long-term bond to take advantage of higher returns.

Ultimately, understanding interest rates is a key component of financial literacy, and it can help you make more informed decisions about your money.

Types Of Interest Rates

Interest rates come in a variety of types, each with its own set of rules and implications. Understanding the different types of interest rates is crucial for making sound financial decisions, such as deciding whether to take out a fixed or variable interest rate loan, or whether to invest in a bond with a high or low interest rate.

Some of the most common types of interest rates include –

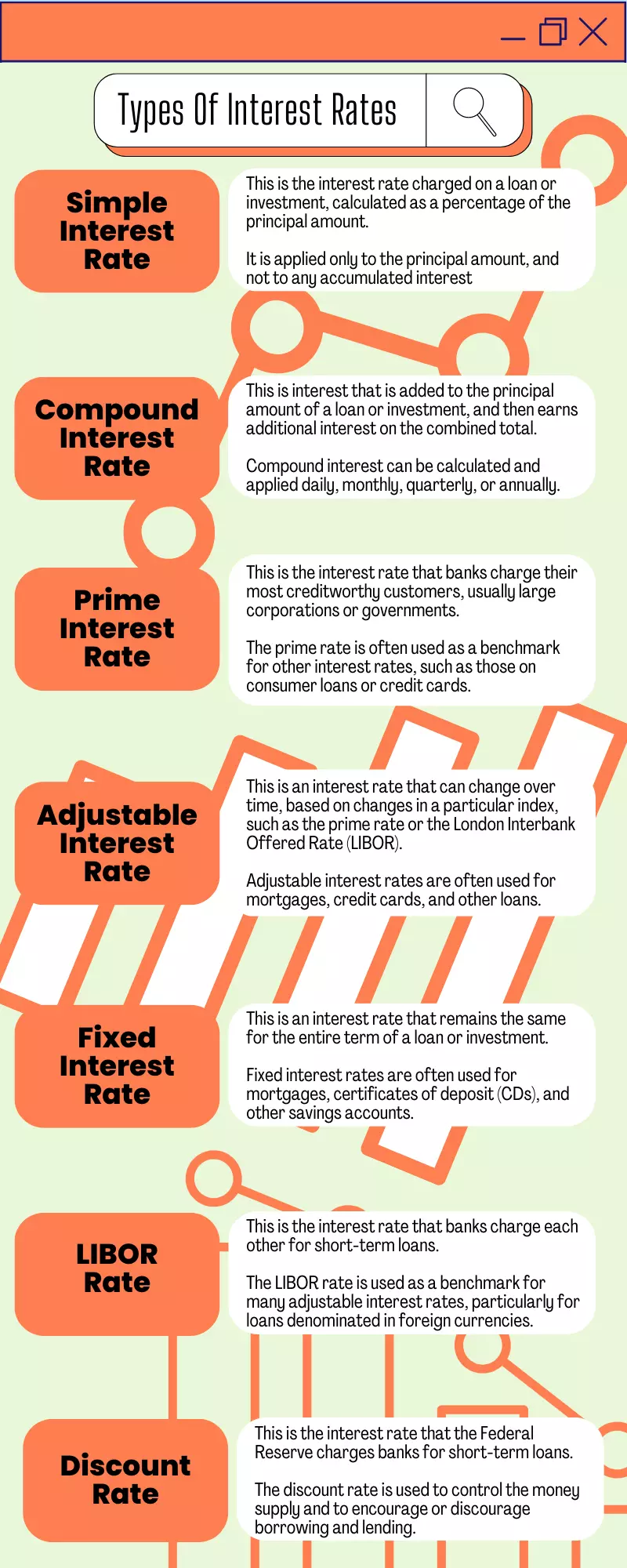

- Simple interest rate: This is the interest rate charged on a loan or investment, calculated as a percentage of the principal amount. It is applied only to the principal amount, and not to any accumulated interest.

- Compound interest rate: This is interest that is added to the principal amount of a loan or investment, and then earns additional interest on the combined total. Compound interest can be calculated and applied daily, monthly, quarterly, or annually.

- Prime interest rate: This is the interest rate that banks charge their most creditworthy customers, usually large corporations or governments. The prime rate is often used as a benchmark for other interest rates, such as those on consumer loans or credit cards.

- Adjustable interest rate: This is an interest rate that can change over time, based on changes in a particular index, such as the prime rate or the London Interbank Offered Rate (LIBOR). Adjustable interest rates are often used for mortgages, credit cards, and other loans.

- Fixed interest rate: This is an interest rate that remains the same for the entire term of a loan or investment. Fixed interest rates are often used for mortgages, certificates of deposit (CDs), and other savings accounts.

- LIBOR rate: This is the interest rate that banks charge each other for short-term loans. The LIBOR rate is used as a benchmark for many adjustable interest rates, particularly for loans denominated in foreign currencies.

- Discount rate: This is the interest rate that the Federal Reserve charges banks for short-term loans. The discount rate is used to control the money supply and to encourage or discourage borrowing and lending.

One important type of interest rate is the real interest rate, which is adjusted for inflation and reflects the true cost of borrowing or the true return on lending.

This is important to consider, as high inflation can erode the value of a loan or investment, reducing the real return.

Another important type of interest rate to be aware of is the Annual Percentage Rate (APR), which includes all fees and charges associated with borrowing and is expressed as an annual percentage rate.

The APR is especially relevant when comparing loans or credit cards, as it allows you to compare the true cost of different options.

By understanding the different types of interest rates, you can make more informed decisions about borrowing and investing, which can have significant financial implications over time.

For example, knowing the difference between fixed and adjustable interest rates can help you decide which type of mortgage is best for you, while understanding the real interest rate can help you assess the true value of an investment.

Overall, understanding the nuances of interest rates can help you save money, avoid costly mistakes, and make the most of your financial resources.

Factors That Influence Interest Rates

Have you ever wondered why interest rates change over time? The answer lies in the many factors that influence interest rates, which can range from global economic conditions to the actions of central banks.

Understanding these factors is essential for making informed financial decisions, as changes in interest rates can affect the cost of borrowing and the return on investment.

One of the most significant factors that influence interest rates is the state of the economy. When the economy is growing, interest rates tend to rise, as banks and lenders expect increased demand for borrowing and a corresponding increase in inflation. Conversely, when the economy is in recession, interest rates tend to fall, as the demand for borrowing decreases and there is less inflationary pressure.

Another factor that influences interest rates is the actions of central banks, such as the Federal Reserve in the United States. By adjusting short-term interest rates, central banks can influence the borrowing costs for banks and other financial institutions, which can in turn affect the rates offered to consumers and businesses.

Other factors that influence interest rates include inflation rates, geopolitical events, and market forces such as supply and demand. For example, a sudden surge in demand for loans could lead to higher interest rates, while a decrease in demand could lead to lower rates.

By understanding the many factors that influence interest rates, you can better anticipate changes in borrowing and investment costs, which can have significant implications for your financial future.

For example, if you anticipate that interest rates will rise, you may want to consider locking in a fixed-rate loan before the rates increase.

Conversely, if you expect rates to fall, you may want to delay taking out a loan or invest in long-term bonds that offer higher returns.

Ultimately, understanding the complex web of factors that influence interest rates is a key component of financial literacy and can help you make better financial decisions.

Relationship Between Interest Rates And Borrowing/Lending

Interest rates play a critical role in the relationship between borrowers and lenders, as they determine the cost of borrowing and the return on lending.

Whether you’re taking out a loan, investing in bonds, or saving money in a bank account, the interest rate you receive or pay can have a significant impact on your financial situation.

When interest rates are low, it can be an ideal time to borrow money. This is because the cost of borrowing is lower, making it more affordable to take out a loan or mortgage.

Conversely, when interest rates are high, it can be more expensive to borrow money, which can discourage borrowing and lead to slower economic growth.

For lenders, interest rates also play an important role in determining the return on investment. When interest rates are low, it can be more challenging to earn a significant return on investments such as bonds or savings accounts.

Conversely, when interest rates are high, it can be easier to earn a higher return on investments.

For example, let’s say you take out a mortgage with a fixed interest rate of 3%. This means that you’ll pay 3% interest on the amount you borrow for the duration of the loan. If interest rates later increase to 5%, you could potentially save money by refinancing your mortgage to a lower interest rate.

I’ve also created a guide on what things you need to do for budgeting for a new house.

On the other hand, if you had invested in a bond with a high interest rate, you could earn a significant return on your investment.

In short, the relationship between interest rates and borrowing/lending is a crucial aspect of personal finance, and understanding this relationship can help you make better financial decisions.

Whether you’re looking to take out a loan, invest in bonds, or save money in a bank account, paying attention to interest rates can help you make the most of your financial resources.

Impact Of Interest Rates On The Economy

Interest rates play a significant role in shaping the overall state of the economy, as they affect borrowing costs, consumer spending, and investment decisions. When interest rates change, it can have a ripple effect throughout the economy, impacting everything from the housing market to the stock market.

One of the primary ways that interest rates affect the economy is through their impact on borrowing costs. When interest rates are low, it can be more affordable for consumers and businesses to take out loans, which can encourage spending and stimulate economic growth.

Conversely, when interest rates are high, borrowing costs can become prohibitively expensive, leading to reduced spending and slower economic growth.

Interest rates can also impact the housing market, as they affect the affordability of mortgages. When interest rates are low, it can be easier for people to buy homes, which can stimulate the housing market and the broader economy.

Conversely, when interest rates are high, it can become more difficult for people to afford homes, leading to a slowdown in the housing market.

In addition to their impact on borrowing costs and the housing market, interest rates can also affect investment decisions.

When interest rates are low, investors may be more likely to invest in stocks or other assets, as they may offer higher returns.

Conversely, when interest rates are high, investors may be more likely to invest in bonds or other fixed-income securities, which can offer more predictable returns.

Overall, the impact of interest rates on the economy is complex and multifaceted. By understanding how interest rates affect different aspects of the economy, you can gain insights into the broader economic landscape and make informed financial decisions.

Whether you’re a consumer, investor, or business owner, paying attention to interest rates can help you navigate the ever-changing economic landscape.

Conclusion

Congratulations! You’ve taken the first step in understanding interest rates and their impact on your financial well-being.

By taking the time to learn about the different types of interest rates, the factors that influence them, and their relationship to the broader economy, you’re already ahead of the game.

So, what can you do with this knowledge?

The answer is simple: use it to your advantage. By understanding how interest rates impact your borrowing costs, investment returns, and overall financial situation, you can make more informed decisions and take control of your financial future.

Think of it this way: every dollar you save on interest is a dollar you can put towards your goals, whether that’s paying off debt, saving for retirement, or investing in your future.

By staying informed about interest rates and taking advantage of low rates whenever possible, you can save money, build wealth, and achieve your financial dreams.

So, take this information and run with it. Stay up-to-date on interest rate trends, shop around for the best rates on loans and credit cards, and explore different investment options to find those with the best potential returns.

With a little bit of effort and a lot of determination, you can use your knowledge of interest rates to build a brighter financial future for yourself and your family.